Cap Table Management

Centralized Cap Table Management for CPA & Advisory Firms

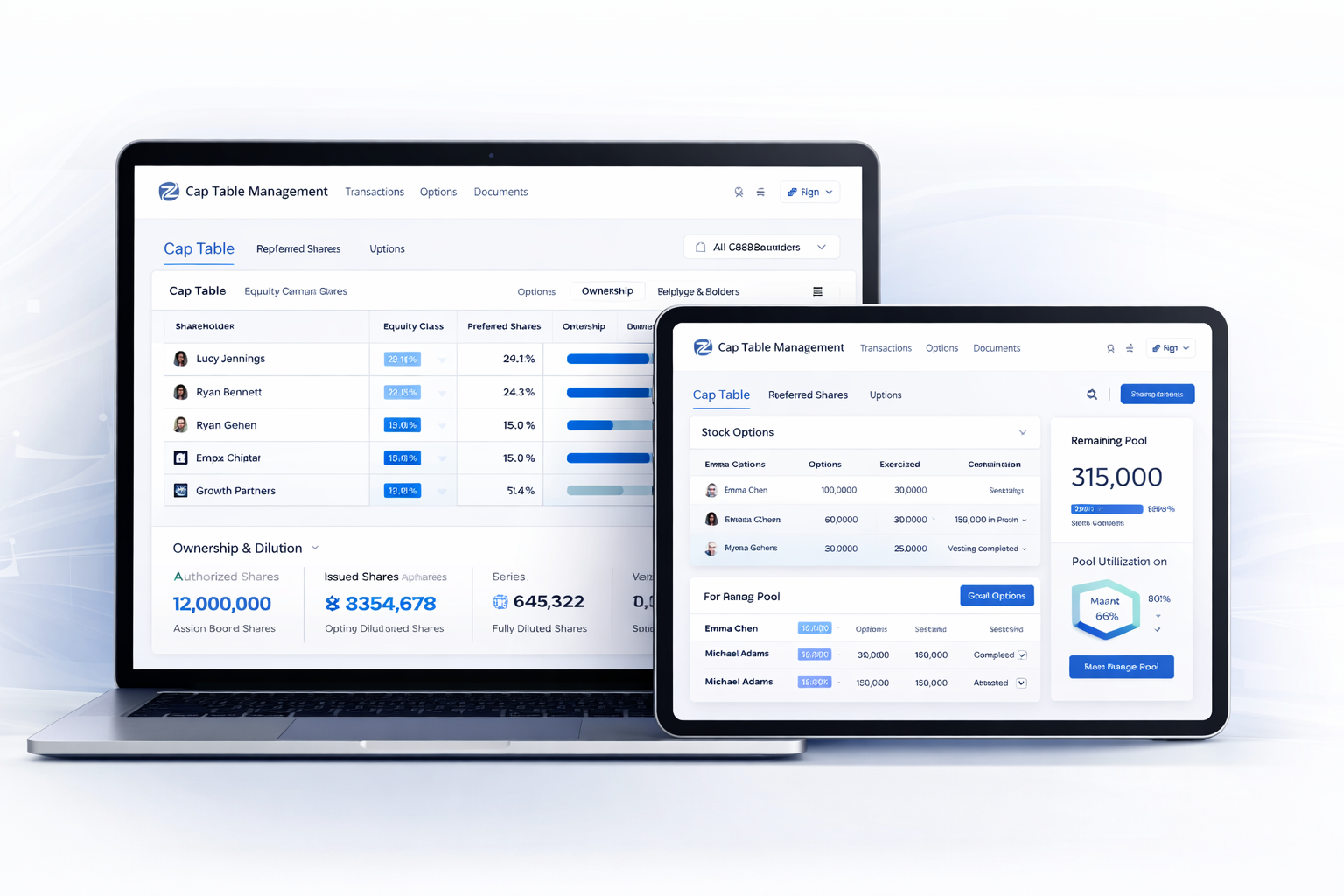

Simplify cap table management, ASC 820 & IRS 409A valuations, and generate audit-ready reports with confidence.

ZimbsTech – Innovative Software Solutions for Modern Businesses

Simplify cap table management, ASC 820 & IRS 409A valuations, and generate audit-ready reports with confidence.

ZT Valuation simplifies cap table management by providing a centralized, real-time view of company ownership. Track shareholders, equity issuances, and option grants with complete accuracy—without spreadsheets or manual errors. Designed for founders, finance teams, and CPA firms who demand precision and audit-ready records.

Field Experience

Done Around World

Client Satisfaction

Established On

Response Time

+91 890 5544 504

contact@zimbstech.com

ZimbsTech 402, Horizon Trade Center (HTC), Nr. Vaishnodevi Circle, Ahmedabad, Gujarat, India